Car accidents can happen to anyone, and sometimes they are our fault. When this happens, it’s important to understand how car insurance works. Many people feel confused about what to do next and how it will affect their insurance. In this article, we will break down the key points about car insurance when you’re at fault.

We’ll explain what to do after an accident, how claims work, what your insurance covers, and how it might impact your rates. By the end, you’ll have a clear understanding of your responsibilities and options, making it easier to handle an accident if it ever happens to you.

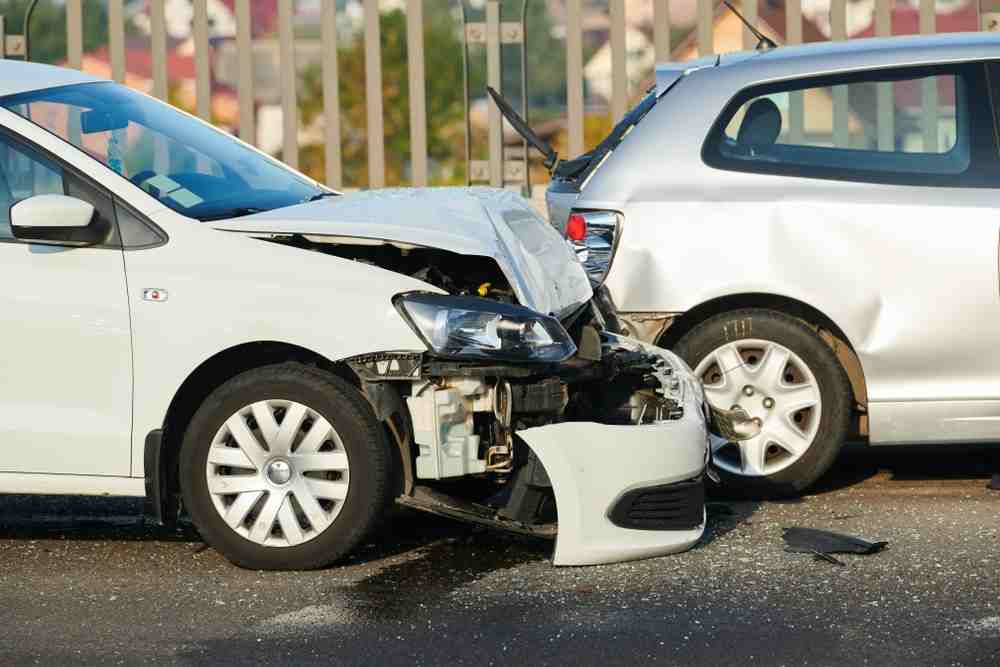

What is Fault in Car Accidents?

In the context of car accidents, fault refers to the party deemed responsible for causing the incident. Determining fault is crucial as it influences insurance claims and liability for damages. In many cases, fault is straightforward; for example, a driver who rear-ends another vehicle typically bears full responsibility.

However, the process can become complicated depending on state laws and specific circumstances surrounding the accident. In fault-based states, the at-fault driver is liable for covering damages incurred by other parties, which may include medical expenses and property damage.

Conversely, in no-fault states, each driver’s insurance covers their own damages regardless of who caused the accident. Additionally, situations involving shared fault may lead to comparative negligence assessments, where each driver’s degree of fault affects how damages are compensated.

What Happens if You Are At Fault in a Car Accident?

If you are at fault in a car accident, the implications depend largely on the state you reside in and your insurance coverage. In fault states, you (or your insurance) are responsible for covering the damages incurred by the other driver, which may include medical bills, vehicle repairs, and other related expenses.

Your liability insurance kicks in to handle these costs, but you may also need to pay a deductible if you claim for damages to your own vehicle under collision coverage.

Additionally, being at fault typically leads to an increase in your insurance premiums upon renewal, as insurers often raise rates for drivers who have caused accidents. In contrast, no-fault states require each driver’s insurance to cover their own damages regardless of who is at fault, although liability coverage is still necessary for property damage claims against the at-fault driver

What Damages Are Covered if You Cause a Car Accident?

If you cause a car accident, several types of damages may be covered by your insurance, depending on your policy and the circumstances of the accident:

- Bodily Injury Liability: This covers medical expenses for injuries sustained by other parties involved in the accident, including hospital bills and rehabilitation costs.

- Property Damage Liability: This covers damages to the other party’s vehicle or property, such as fences or buildings damaged in the accident.

- Collision Coverage: If you have collision coverage, it will pay for repairs to your own vehicle after an accident, regardless of fault. However, you will need to pay your deductible first.

- Lost Wages: If the injured parties miss work due to the accident, your liability insurance may cover their lost wages.

- Pain and Suffering: Compensation for physical pain and emotional distress experienced by the injured parties may also be claimed.

In most cases, your insurance will handle these claims up to the limits of your policy. If damages exceed those limits, you may be personally liable for the additional costs.

What Should You Do After an At-fault Car Accident?

After an at-fault car accident, follow these key steps:

- Stay Calm and Check for Injuries: Ensure you and your passengers are safe. If anyone is injured, call 911 immediately.

- Move Vehicles (if possible): If your car is drivable, move it to a safe location away from traffic. Turn on hazard lights to alert other drivers.

- Call the Police: Report the accident to law enforcement, even if it’s minor. They will document the scene and file a report.

- Exchange Information: Collect names, contact details, insurance information, and vehicle details from all parties involved.

- Document the Scene: Take photos of the vehicles, damage, and the accident scene to support your insurance claim.

- Notify Your Insurance Company: Inform your insurer about the accident as soon as possible to begin the claims process. Provide them with all necessary documentation.

- Avoid Admitting Fault: When discussing the accident with others, stick to the facts and avoid admitting fault or discussing blame.

Following these steps can help you manage the aftermath of an accident effectively and ensure that your insurance claim is processed smoothly.

What Happens if You Are Partially at Fault in a Car Accident?

If you are partially at fault in a car accident, the outcome depends on the laws of your state regarding comparative negligence. In many states, including California and Georgia, you can still recover damages, but the amount will be reduced based on your percentage of fault.

For example, if you are found to be 30% at fault for an accident that results in $10,000 in damages, you would only be eligible to receive $7,000. However, if you are deemed 50% or more at fault in states with modified comparative negligence laws, you may be barred from recovering any damages.

Additionally, being partially at fault can lead to increased insurance premiums and may affect your coverage options in the future. It’s advisable to consult with a legal professional to navigate the complexities of your specific situation and ensure your rights are protected.

How Much Does Insurance Go Up After an At-Fault Accident?

After an at-fault accident, car insurance premiums typically see a significant increase, which can vary widely based on several factors. On average, drivers may experience a rate hike of around 41% following an at-fault incident, although increases can range from 26% to as high as 71% depending on the insurance provider and the specifics of the accident, such as its severity and costs involved. For instance, a minor fender bender might result in a smaller increase compared to a serious collision with substantial damages or injuries.

Why Electric Car Insurance Costs More

Moreover, the duration for which these increased rates apply generally spans three to five years, during which insurers may reassess risk based on driving records and claim history. In some cases, insurers offer accident forgiveness programs that prevent rate hikes after the first at-fault accident, but this benefit varies by company and often requires prior enrollment. Overall, it is advisable for drivers to shop around for quotes from different insurers post-accident, as rates can differ significantly among companies.

Claims Process After an Accident

After a car accident, the claims process involves several key steps:

- Notify Your Insurer: Contact your insurance company as soon as possible to report the accident. Most insurers require notification within a specific timeframe, often within 24 to 48 hours.

- Fill Out a Claim Form: Obtain and complete the claim form provided by your insurer. Be sure to include all relevant details about the accident.

- Gather Documentation: Collect necessary documents, such as a police report, photos of the accident scene, and any witness statements. These will support your claim.

- Claim Investigation: The insurer will assign a claims adjuster to investigate the claim. They will assess the damage and determine liability based on the information provided.

- Claim Approval and Payment: If your claim is approved, you will receive compensation for the damages according to your policy terms. This may involve direct payment to a repair shop or reimbursement for expenses incurred.

Do You Need Insurance to Purchase a Used Car?

It’s crucial to provide accurate information throughout the process to avoid delays or potential claim denial.

Saving Money on Car Insurance

Saving money on car insurance after being at fault in an accident can be challenging, but it’s not impossible. Here are some strategies that may help:

- Review Your Policy: Look at your current coverage and see if there are any adjustments you can make that could lower your rates. This might include increasing your deductible or dropping certain coverages that may no longer be necessary.

- Check for Discounts: Many insurance companies offer various discounts, such as for safe driving, multiple policies, or having a car with safety features. Make sure you’re taking advantage of all the discounts you’re eligible for.

- Drive Safely: By maintaining a clean driving record after the accident, you can gradually reduce the impact of the accident on your premiums. Some insurers offer accident forgiveness programs that might prevent your first accident from affecting your rates.

- Take a Defensive Driving Course: Some insurers offer discounts to drivers who complete an approved defensive driving course. This can also help to improve your driving skills and reduce the likelihood of future accidents.

- Shop Around: Don’t hesitate to shop around for new quotes from different insurers. Rates can vary significantly between companies, and you might find a better deal elsewhere.

- Bundle Policies: If you have multiple insurance policies, consider bundling them with the same provider for a discount. This can include home, renters, or other types of insurance.

- Consider Usage-Based Insurance: If you don’t drive often, a usage-based insurance program could save you money. These programs base your rates on how much you drive and how safely you drive.

Remember, the key is to demonstrate to insurers that you are a responsible driver, despite the at-fault accident. Over time, this can help mitigate the increase in your premiums.

FAQs

Q 1. What should I do immediately after an at-fault accident?

Ans. Immediately after an at-fault accident, ensure everyone’s safety and call emergency services if there are injuries. Exchange information with the other party, document the scene with photos, and notify the police. Contact your insurance company to report the accident as soon as possible.

Q 2. Can I still file a claim if I am at fault in an accident?

Ans. Yes, you can still file a claim with your insurance company if you are at fault. Your liability coverage will pay for the other party’s damages, and collision coverage (if you have it) will cover your vehicle’s repairs, minus your deductible.

Q 3. Will my insurance rates go up even if the accident damage is minor?

Ans. Yes, insurance rates can still go up after an at-fault accident, even if the damage is minor. The increase depends on your insurer’s policies, your driving history, and the specifics of the incident.

Q 4. How can I dispute a fault determination by my insurance company?

Ans. To dispute a fault determination, gather evidence such as witness statements, photos, or videos that support your case. Present this information to your insurer and, if necessary, seek legal advice or mediation.

Q 5. What is the difference between at-fault and no-fault when it comes to insurance claims?

Ans. In at-fault states, the driver who caused the accident is responsible for damages. In no-fault states, each driver’s insurance covers their own injuries regardless of who caused the accident.

Q 6. How long will an at-fault accident stay on my insurance record?

Ans. The duration varies by state, but typically, an at-fault accident can stay on your insurance record for three to five years.

Q 7. Can I switch insurance providers after an at-fault accident?

Ans. Yes, you can switch insurance providers after an at-fault accident, but be aware that your accident history will be considered by the new insurer when determining your rates.

Conclusion

In conclusion, understanding how car insurance works when it’s your fault is important for every driver. If you cause an accident, your liability insurance will help pay for the other person’s damages and injuries. If you have collision coverage, it can also help fix your own car.

Remember that being at fault can lead to higher insurance rates, but some companies offer programs to keep your rates from going up after an accident. If you’re unsure about your coverage or what to do after an accident, don’t hesitate to reach out to your insurance agent or a lawyer for help.

Milo Thistlethwaite is an auto insurance guru with over 8 years of experience in the industry. Holding a CPCU (Chartered Property Casualty Underwriter) certification, Milo is passionate about helping drivers find the best coverage for their needs. As an author on the ‘Insurance Guy’ blog, Milo writes clear, easy-to-understand articles about auto insurance.